GST India: GSTR-1 Demystified

GST brings the concept of uploa...: GSTR-1 Demystified GST brings the concept of uploading business transaction data versus the existing system of filing summary informat...

Sunday, 18 June 2017

GSTR-1 Demystified

GST brings the concept of uploading business

transaction data versus the existing system of filing summary information. GSTR-1

refers to filing of outward supply details by a regular dealer registered in

GST on or before 10th of subsequent month.

These details get

auto-populated to counterparty (buyer) as GSTR-2A on 11th. Adherence

to dates is of prime relevance since apart from late fees (Rs 100 per day up to

a maximum of Rs 5,000), missing deadlines leads to changes in return filing

flow. Concept of return revision has been done away with and changes if any

have to be done at invoice level.

Return may be filed by user in following

methods:

- Enter invoice data directly in GST portal – requires high speed and reliable internet connectivity and suitable for small business. Ex: 50 to 100 invoices per month

- Enter data in Excel template provided by GST >> import into offline utility >> convert to uploadable file (.json) >> Login to GST portal, browse and upload – multi-step process, suitable for business maintaining data in Excel or using billing or Point of Sale solutions (not integrated with GST) which can provide excel output/summary

- Use Accounting/ERP software and upload data directly to GST – connected solution: convenient and preferred method for most business, as the ERP would handle most of the backend activities (upload/download/session) with minimal physical presence of owner required.

Principal categories of information to be furnished as

part of GSTR-1 are:

·

Sales

(Local/Interstate, Taxable/Exempt/Nil Rate, B2B and B2C)

·

Exports

·

Debit and Credit

notes

·

Advances

·

Revisions for earlier

tax period

·

Other Info (Turnover,

HSN Summary, Invoice series etc.)

Below is the table-wise details of information to be furnished:

1.

GSTIN

– The 15 digit GST Registration number of the business entity Ex: 27ARETY3456J1Z1

2(a). Legal name of the business Ex: One97 Communications

(b). Trade

name of the business Ex:

Paytm

3(a). Turnover of previous financial year (2016-17)

(b). Turnover of April-May-June 2017

Aggregate turnover here refers to combined

turnover across India for the PAN, and includes exempt supplies and exports.

This does not include inward supplies on which tax is paid on reverse charge

basis.

4. Taxable outward supplies to registered business

Taxable

supplies are to be reported in Table 4 (A to C) and thereby this table does not

include details of supplies of Nil Rated / Exempt or non-GST goods even if

supplied to B2B customer. However if an invoice has at least one taxable

item/service it will be reported here although other items may be Nil/exempt. Supplies

done to SEZ or SEZ developer and sales of deemed export nature although of

taxable and B2B nature will not participate in Table 4. Across all tables when

invoice information is reported, rate-wise breakup is to be provided. If there

are multiple items (Ex: 15) in a single invoice but falling in 3 rates, the

invoice information will be furnished in 3 lines.

4A.

Outward supplies to registered business

Explanation:

Taxable sales done to business (B2B) customers having GSTIN and such service is

not classified as reverse charge. Does not include B2B sales done through

e-commerce operators.

4B.Outward

supplies attracting reverse charge

Explanation:

Sales done to business (B2B) customers having GSTIN of those services

classified as reverse charge. Ex: Goods Transport Agency services, Legal services,

Rent-a-cab services etc.

4C.

Outward supplies made through e-commerce operators

Explanation:

Sales done to business (B2B) customers having GSTIN but done through e-commerce

operators like Amazon, Flipkart, e-Bay, Indiamart etc. Sales have to be

provided segregated e-commerce operator wise.

5. Taxable Inter-state B2C supplies more than

Rs.2.5 lakhs

Only taxable supplies will be reported in this

table. (All sales of Nil Rated / Exempt / Non-GST goods or service to

interstate consumers will not participate here).

5A. Inter-state B2C supplies more than Rs.2.5

lakhs

Explanation:

Interstate sales done to consumers (B2C) and the invoice value is more than Rs

2.5 Lakhs (does not include sales done

through e-commerce operator).

5B. Inter-state B2C supplies more than Rs.2.5

lakhs through e-commerce operators

Explanation:

Interstate sales done to consumers (B2C) and the invoice value is more than Rs

2.5 Lakhs and the sale has happened through e-commerce operators (to be

reported e-commerce operator-wise)

6. Zero rated supplies and

Deemed Exports

6A. Exports

Exports

with or without payment (under Bond or letter of undertaking) of tax will be

reported in this section. The Shipping Bill number (13 digit code including six

digits of port code) is not mandatory during saving of invoice and can be

subsequently updated through amendment table. Shipping bill number is to be

mandatorily updated before claiming refund.

6B. Supply to SEZ

Similar

to Exports, supplies to SEZ is zero rated and can be with or without payment of

tax, to be reported here. Shipping bill details will be applicable

when supplied under Bill of Entry.

6C. Deemed exports

Deemed

exports as notified by government to be reported here.

7. Net

B2C outward supplies other than that covered in table 5

All

taxable B2C supplies other than table 5 (interstate B2C > 2.5 lakhs) to be

reported here. Only taxable and B2C supplies of Nil/Exempt/Non-GST will not

participate.

7A. Intra-state B2C supplies

7A (1).

Consolidated rate-wise B2C supplies

All within-state

B2C supplies (irrespective of invoice value) to be consolidated (net of

debit/credit note) and reported here including supplies done through e-commerce

operators.

7A (2).

Consolidated rate-wise B2C supplies done through e-commerce operator

Only those

intra-state B2C sales done through e-commerce operator to be sorted e-commerce

operator wise and reported as consolidated values (net of debit/credit note).

7B.

Inter-state B2C supplies of value up to Rs 2.5 Lakhs

7B (1).

State-wise details of consolidated rate-wise B2C supplies

All interstate

B2C supplies of invoice value =< 2.5 lakhs to be consolidated (net of

debit/credit note) and reported here including supplies done through e-commerce

operators.

7B (2).

State-wise details of consolidated rate-wise B2C supplies done through

e-commerce operator

8. Nil Rated / Exempt /

Non-GST supplies

Explanation: This table captures

net sales (after debit / credit note adjustments) of Nil Rated, Exempt and

non-GST outward supplies and the information is to be further bifurcated as

B2B/B2C and as inter/intra state. All ‘Bill of Supply’ having only Nil / Exempt

/ Non-GST supplies are to be reported in this section.

8A.

Interstate B2B supplies of Nil/Exempt/Non-GST goods/service

8B.

Intrastate B2B supplies of Nil/Exempt/Non-GST goods/service

8C.

Interstate B2C supplies of Nil/Exempt/Non-GST goods/service

8D.

Intrastate B2C supplies of Nil/Exempt/Non-GST goods/service

9. Amendments, Debit and

Credit Notes

Explanation: As stated earlier,

in GST regime there is no provision for return revision and invoices of earlier

tax period entered erroneously (Ex: clerical error) can be corrected through

amendment table by re-uploading the rectified information. Amendment to invoice

data is subject to following conditions:

·

The invoice / Debit / Credit Note is not already

accepted by buyer

·

The invoice / Debit / Credit Note is not already

amended / modified earlier

·

The last period in which any amendment can be

performed is the September return of next financial year or filing of annual

return whichever is earlier

9A.

Invoice amendment

Provision to enter corrected

information pertaining to invoices uploaded & filed in earlier tax periods.

This table can also be used for updating shipping bill details against an

export invoice uploaded in earlier tax period.

9B.

Debit/Credit notes and Refund voucher

Debit and Credit notes issued

against invoices of current or earlier tax periods (not earlier than April month

of the FY to which it belongs) are added in this section. Refund

vouchers are also to be reported here.

(Refund voucher: when advance is received

(receipt voucher) form buyer and subsequently the supply does not happen, supplier to issue a refund voucher)

9C.

Amendment to Debit or Credit note and refund voucher

Corrections to Debit / Credit

notes and Refund vouchers issued in earlier tax period principally to rectify

clerical errors.

10. Amendments to B2C

supplies reported in Table 7

This section refers to

corrections to be incorporated to consolidated B2C sales reported in earlier

tax periods. The information needs to be bifurcated state-wise (Place of

supply) and between e-commerce and non-ecommerce sections.

10A.

Revision of Intrastate B2C supplies of earlier tax periods (including

e-commerce)

10A (1).

Revision of Intrastate B2C supplies of earlier tax periods made through

e-commerce operators

10B.

Revision of Interstate B2C supplies of earlier tax periods (including

e-commerce)

10B (1).

Revision of Interstate B2C supplies of earlier tax periods made through

e-commerce operators

11. Advances received,

adjusted and amended

Another unique provision of GST,

borrowed from existing service tax laws is the requirement to report advances

received from buyer for future supplies and pay tax liability on them. Subsequently

when the invoicing happens, the tax liability paid earlier can be used to

set-off the liability resulting from invoice.

I) Information for current tax

period

11A. Advance received in current tax period but not

invoiced

Consolidated value of advances

received in current month against which no invoice has been raised (or

partially raised) is to be reported in this section with state-wise and rate-wise breakup.

11A (1).

Intrastate supplies

11A (2).

Interstate supplies

11B.

Advances of earlier tax period adjusted in current tax period

This table refers to reporting of

adjustment of liability in invoices raised in current period against liability

discharged on advance in earlier tax period.

11B (1).

Intrastate supplies

11B (2).

Interstate supplies

II)

Amendment to information furnished in tables 11A and 11B in earlier tax periods

Amendments if any to information

furnished in earlier tax period in Table 11A and 11B to be provided here.

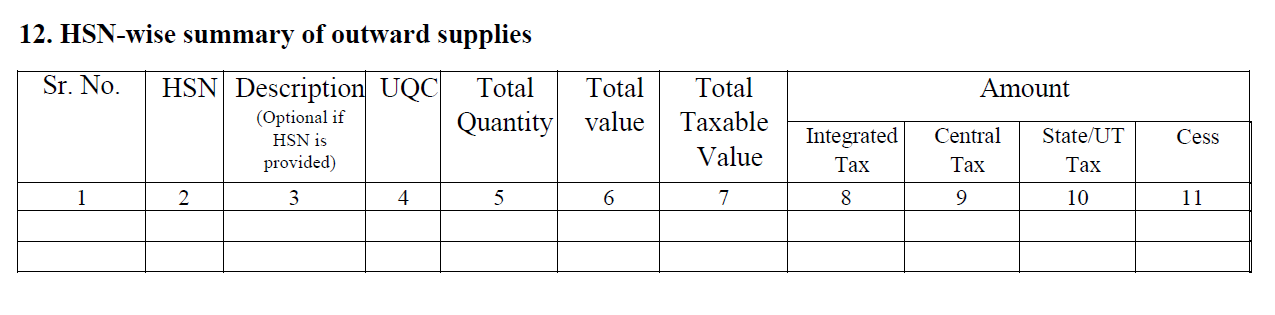

12. HSN Summary

The Table is a provision to

report HSN (Harmonized system of nomenclature) / SC (service code) wise outward

supplies summarized for the return period. For stock items,

the quantity details along with applicable unit of measure also needs to be

reported. For business with turnover < 1.5 crore, HSN is optional and

instead description of goods may be provided.

13. Document series

This section is for reporting the

different voucher series being maintained by business for each document nature

(Ex: B2B invoice, retain invoice, Debit/Credit notes,

Receipt/Refund/Payment vouchers etc.). The number of vouchers issued/cancelled

in the current return period is to be reported.

Conclusion:

GSTR-1 invoices can be uploaded from the beginning of the month till 10th

of subsequent month. The return has to be digitally signed and submitted on or

before 10th of subsequent month. Dongle based digital signature or

Aadhaar based e-sign or EVC (electronic verification code) based signing is

permitted. Taxpayer may also assign a Tax Return Preparer on GST portal and

authorize him to conduct all tax compliance activities. On 11th the

supplies get auto-drafted to buyer and he has option to accept / reject /

modify the supplies and also add any missing invoice in his GSTR-2. Buyer’s decisions are communicated back to

supplier in GSTR-1A, filing of which is optional. Final summary of outward

(GSTR-1) and inward (GSTR-2) and the resultant tax payable is generated by GST

system as GSTR-3. Taxpayer has to discharge his liability and file GSTR-3

latest by 20th.

As is evident, delay in filing of outward details beyond 10th

will result in supplies not getting auto drafted to buyers and thereby

impacting credit flow. Taxpayers need to

therefore adopt an effective ERP solution that assists in addressing these

nuances.

(Views expressed are purely personal and do not represent any organization. This article is based on publicly available information and strictly for education purpose only)

Saturday, 10 December 2016

Impact of GST on E-commerce

E-commerce in India:

Market place model: An

asset light model wherein the e-commerce firm merely acts as a platform and

connects buyers and sellers and does not own any inventory. 100% FDI (Foreign

Direct Investment) is allowed.

Ex:

Amazon, Flipkart, Snapdeal, eBay etc.

Inventory based Model:

The e-commerce firm owns the inventory of goods and services and sells to the

consumers directly. No FDI allowed.

Ex:

Bigbasket, Jabong

Taxation blues:

Today

e-commerce in India is mired in a host of taxes: VAT / CST / Service Tax / TDS

with more than one tax applicable on any given transaction. Involvement of

logistics / reverse logistics, advertising & promotion services, goods like

software, music, e-books etc. makes it hard to differentiate Goods &

Services component of each transaction.

Also, grey areas have emerged due to e-commerce players who have adopted

marketplace model are having own warehouses to store the inventory. Although

there is visible value addition by e-commerce players no VAT is being paid by

them. This has resulted in many disputes with state commercial tax departments.

Karnataka has been insisting on these warehouses to be registered under VAT and

e-commerce players be considered as consignment agents and be made to pay VAT.

Several states (Ex: Delhi, Rajasthan) have insisted on separate disclosures by

dealers of online transactions due to concerns of such sales getting

under-reported. Uttar Pradesh has imposed several restrictions (declaration

form) on interstate purchase of goods worth more than Rs 5,000 through

e-commerce. States like Uttarakhand, Bihar, West Bengal, Himachal Pradesh and

Uttar Pradesh have levied entry tax ranging from 5 to 10% on goods purchased

interstate through e-commerce platforms.

E-Commerce in GST:

Many

e-commerce firms have welcomed GST since for the first time there is a legal

framework that defines ‘electronic commerce’ and

‘electronic commerce operator’. Although the draft model law is far

from being comprehensive, it is expected to evolve and attain maturity.

Business Process Impact:

Outward Supply: With

GST, uniformity in compliance across India is ensured, thus e-commerce sellers

can look for markets beyond state boundaries without the hassles associated

with complying to state specific rules (Ex: Declaration Forms, Way Bills) and

taxes (Ex: Entry Tax).

Compliance: All

sellers on e-commerce platforms will have to obtain GST registration

irrespective of turnover meaning increased compliance vis-à-vis offline

sellers. Fulfillment centre of e-commerce to be registered as additional place

of business by sellers and stock transfer will be treated as taxable supply

leading to cash flow issues. Both the vendor and e-commerce operator will have

to report supplies and will be cross-matched. Any supply reported by operator

but not by vendor will be added to the liability of the vendor.

Tax Invoice: Tax invoices need to be physically or

digitally signed (digital signature ink).

Schemes and Discounts: All

discounts will have to be explicitly mentioned in invoice and post supply

discounts by market place to a seller (promotions) will have to be more

explicit and be agreed in advance. As Freebies will also be taxable, sellers

will need to tweak their offerings.

Logistics: With

e-commerce operators expected to collect a portion of GST and pay to the

government on behalf of the seller (Tax Collected at source at 2%) there is a

new paradigm getting established. The TCS deducted on aggregate sales for the

month (sales less sales return) will be credited to electronic cash ledger of

seller. E-commerce players providing

their own logistics services will be able to quickly adopt to this new reality

as cash flow happens through their network. With nearly two third sales

happening through CoD (Cash on Delivery) model, if a third party logistics

provider is involved, the cash flows have to be now tweaked to flow back to the

e-commerce operator to enable deduction of tax. Alternatively, the tax amount of

CoD orders has to be now deducted from pre-paid sales.

With many e-commerce firms following weekly settlement for sellers, the TCS needs to be deducted in such invoices and filed by e-commerce operator in their GSTR-1.

(Note: This is not to be confused with 10% income tax TDS (on commission) which sellers are supposed to deduct while paying commission to e-commerce operator. This in practice is currently deducted by operator and paid to income tax department on behalf of seller.)

Reverse Logistics:

With high prevalence of goods returns (15-20%) and cancellations, reverse

logistics also needs to be more robust. Raising of credit note is not a very

prevalent practice currently, but will have to be adopted for accurate

depiction of tax liability.

High

volume of transactions (200 to 300 per day), thin margins, and increased

compliance (upload & matching, advance tax) mean, only adoption of a robust

IT solution can guarantee smooth business operations.

Depiction of Process Flow:

Below

diagram illustrates the flow of orders and funds in the GST era:

Fulfillment

of Cash on Delivery order by an e-commerce seller through a 3PL provider is

illustrated. In this case fulfillment is by seller and not the marketplace.

Order and Goods Flow:

Cash Flow:

Let

us assess the impact using an example as below:

M/S

SLV Traders deals in Metallic Sports Water Bottles. He purchases them directly

from manufacturer and sells on e-commerce platforms through the fulfillment

model.

Assumptions:

For the sake of this illustration, it is assumed that the products are charged

at 5% VAT, and goods charged at lower VAT rate are likely to be charged at

lower rate of GST as well (12%). For the sake of comparison the purchase and

sale price are kept same in both tax regimes.

Current Tax Regime:

GST Regime:

Comparison:

Findings:

·

Despite similar purchase and sale price in both VAT and GST regime, the

profitability is much higher in GST. This is mainly due to a number of taxes

(Central Excise and Service Tax) that formed costs in VAT regime will be

available as inputs in GST regime.

· In the above illustration although the GST rate at 12% is much higher

than VAT rate of 5%, the net tax payable in GST regime is lower by 9% due to

elimination of cascading effect.

· In the medium to long term due to competition the profit margin levels

may come down to pre-GST levels and thus the benefits of lower cost and lower

tax payable will be passed onto end customer.

Impact Assessment:

The

earlier draft model law talked principally of two categories of online players,

i.e market places and aggregators of services under their brand name (Ex: Ola/Uber/IRCTC/Makemytrip

etc.). However, many e-commerce players act as both aggregator and marketplace. Other

prevalent e-commerce formats like aggregators of ‘goods’ under their brand (Ex: Quikr/CarTrade/Olx etc.) are not

clearly defined. Many e-commerce firms only act as a meeting place for buyers

and sellers and are not themselves involved in financial transaction (Ex: B2B

players like Alibaba and eBay) and hence collection of tax at source cannot be

applied. A host of job portals (Ex: Naukri.com, Timesjobs), matrimonial

websites (Ex: Shaadi.com, Jeevansaathi.com), restaurant booking (Ex: Zomato),

food delivery (Ex: Swiggy), adventure/vacation booking sites (Ex:

Thrillophilia), hyperlocal delivery (Ex: Grofers, Amazon Now, Zopnow), cab

rentals (Ex: Zoomcar, Myles), digital wallets (Ex: Paytm), music download,

mobile advertising (Ex: InMobi) have innovative business models which cannot be

classified as a pure play marketplace or aggregator. Hence further redefining

of Model draft law is needed.

The

revised draft GST law however has removed the definition of aggregators and

these might get covered under draft rules.

Conclusion:

In

conclusion, the benefits of GST resulting from uniformity in processes across

the country, elimination of cascading effect, boost to economy, legal standing

for e-commerce will far outweigh the glitches pertaining to increased compliance

burden. E-commerce platforms and sellers

will have to make the necessary changes to their IT infrastructure to

accommodate for ‘destination-based-consumption’ regime and to meet new accounting requirements pertaining to Tax

deduction at source. E-commerce sellers will be required to be mandatorily

registered under GST irrespective of turnover. Outward supply reported by

sellers (GSTR-1) will be compared with report of sales by e-commerce operator

(GSTR-8) and any under reporting will be penalized adding to compliance burden.

With many e-commerce unicorns (valuation in excess of 1 Billion US $) emerging

in India (Flipkart, Ola, InMobi, Paytm, Shopclues, Zomato) GST law needs to

encourage such business growth while not compromising on reasonable tax

demands.

Subscribe to:

Comments (Atom)