GST India:

Open API approach

It strategy is at the core of system

design for GST and the approach taken is to provide open APIs for integration

by third party vendors. Taxpayers are expected to interact with GST system

using applications developed by third party vendors (Desktop or app or browser

based) which would be device agnostic (PC, Mobile, Tablet, etc.). Third party

Accounting/ERP solutions or apps would integrate with GST system using secure

APIs based on OAuth 2.0 specifications. A minimalistic G2B portal will also be available for

taxpayers for manual interaction.

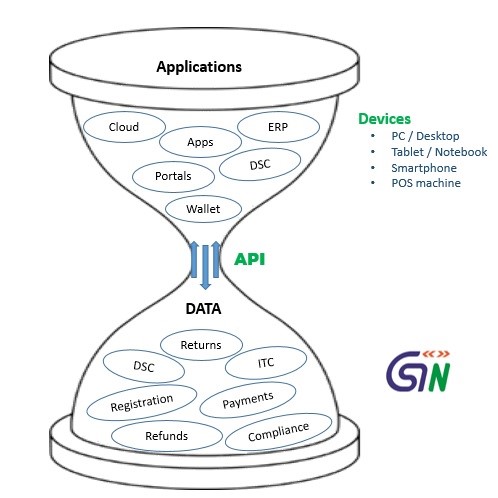

By adopting an hourglass architecture GST system aims to act as a

platform and thereby encourage development of a vibrant GST ecosystem. Various

stakeholders like the taxpayers, Central and State tax departments, Banks,

Payment solutions etc., would thus be

able to connect to GST system using alternate apps, web portals and interfaces

built by third parties. API based platform architecture would enable

automation, divert load from G2B portal besides providing ease of use. Existing

accounting-cum-ERP packages would be able to easily integrate thus enabling the

taxpayers already using such solutions.

GSTN Architecture:

Advantages of API approach:

1.

Taxpayer perspective:

A taxpayer would gain from the plethora of choices in

terms of ERP or Accounting software applications and interfaces available across

devices. For users of existing solutions, integration with GSTN would drive

ease of use and adaptability. Taxpayer may use one or more of the solutions

available in market to suit his requirements without depending on sole G2B

portal for interactions. Commercial (pricing) of products would also be

competitive due to development of healthy ecosystem.

2.

Novelty:

Private

sector enterprises would innovate and bring in novel solutions in areas of

application development (online-offline), scope (return filing, payments,

registration etc.), interfaces, multiple device capabilities and device

integration (POS, micro-ATM, DSC dongle etc.).

3.

Change management:

GSTN by acting as a platform would be in a better

position to handle changes related to tax laws, changes to backend systems and

thereby implement changes without affecting the external stakeholders. This is

in comparison to GSTN acting as a provider of a monolithic, fully integrated

interface wherein any change implementation would necessitate each dependent to

make necessary modifications at his end.

4.

Others:

Individual APIs are easy to

manage, deploy, modify and version rather than making changes to entire application.

And with the kind of scale anticipated (over 3 Billion invoices to be uploaded

every month by 80 Lakh+ dealers across India), APIs allow for load to be

distributed away from G2B portal towards third party applications. APIs provide

for data structure validation and avoid duplication thereby assist in

maintaining single source of truthful data. Security concerns are also

addressed by usage of encapsulation, encryption, user credentials and digital

signatures. As GSTN aims to be self-sufficient in terms of revenue, it is

simpler to charge users as per API consumption patterns.

By envisioning GST system as a

platform, the architects of the system have paved way for a futuristic model

which is not available even in developed countries. Development of a robust

eco-system of application and infrastructure providers is inherent to the

design. A number of stakeholders (Tax authorities, Tax payers, Central &

State governments, Banks, Payment gateways, wallets, DSC / e-sign providers,

apps / ERP firms etc.) are likely to benefit hugely from this approach.

(Views expressed are strictly personal)

hey, your post seemed quite interesting but difficult to understand being a layman. would be glad if it can be explained in much simpler way.

ReplyDelete